Financially Wise

Financially Strong

A Beginner’s Guide to Master the Fundamentals of Personal Finance and Take Control of Your Money

Read sample chapters

Introduction

Everyone is probably familiar with the saying “money doesn’t buy happiness.” While aspects might be true, the importance of money is plain to anyone who doesn’t have enough. Without it, what you have instead is a world of worries, problems, and unhappiness! This I know from personal experience.

Like many others, I started with almost nothing. Sadly, I had no natural talents to use nor were my parents able to help me financially. I therefore accepted I must earn success by working crazy hard and continuously trying to improve myself. When I was young, my simple wish was to have enough money to live comfortably. I didn’t need to be wealthy, only worry-free.

I remember when I started my first job. It automatically made me the breadwinner for my mother and me. My income was ridiculously small, given that I had only a high-school education and zero work experience. After working for a few months, I noticed a pattern. I would run out of money by the third week of each month and my mother, an extremely proud lady, would have to seek a small loan to tide us over to my next payday. This situation continued, much to my mother’s embarrassment, until a bank gave me my first credit card. The limit was small, but that was okay. I only needed a limit large enough to stop borrowing from friends and family.

But after I received the card, my situation didn’t improve. And why would it have? All I did was trade one form of borrowing for another. My month-ends followed a similar pattern. I was paid around the 28th of the month. The first thing I did was pay off my credit card because I hated the thought of owing anyone, even a bank. Then, after paying the monthly bills due, I was out of money. Until my next salary payment, I could only make purchases using my credit card.

It’s funny when you are in the moment and life is happening rapidly around you, the obvious may not be so obvious. One month-end the reality hit me: I was just paid, yet I already had no money! Ideally, you should use your salary to cover your costs for the next month. But there I was paying off old expenses and had no money for expenses for the upcoming thirty days. I describe the expenses as “old” because my credit card bill was for purchases I made weeks ago, and the other bills I paid were for services I had already used.

I kept asking myself, why was I in this situation? I concluded that I just did not know any better. When I entered the workforce, I had gone to school for several years but still knew nothing about one of life’s most important skills: managing my own finances. It was a frustrating moment for me. I faced options about money every day, but I did not know what to do. Eventually, I accepted that I had no reason to be guilty about my lack of knowledge because I had never learned how to make a wise financial decision. If you are near a hot stove, would you touch it? Never. Why? Because you learned it would burn you. You have the knowledge to make a wise choice.

Inexplicably, we often do not approach personal finance as something to be taught and learned. Across a lifetime, we will face endless financial situations that require us to act. The problem is that the wrong choice can cause pain. You often, however, cannot tell, unlike when you touch a hot stove. Put another way, a wrong decision will make you poorer, but owing to a lack of knowledge, you will not have realized it. If you had the knowledge, instinctively you would have made a different choice, like not touching the stove.

Who should read this book?

I wrote this book for people who want to learn how to make wise decisions about their money. And while writing it, I assumed you are as I was: with no money and no clue what to do next.

I do not focus on complex areas of finance, which many of us are unlikely to meet. I am interested in situations and transactions we face regularly. For example, the credit card I obtained was my first loan and serious financial transaction. I remember the lending officer had to explain how it worked. I could not follow anything that was said because realistically they don’t have the time to ensure you understand what you are committing to. At that time, it didn’t matter to me anyway. All I cared about was that the card allowed me to borrow easily. Nothing more. Only much later did I learn about the many pitfalls to avoid when using a credit card.

Financial decisions usually involve understanding detailed rules about a product or transaction. It often requires you to think about legal and taxation aspects as well. But good news: I did not include any of these complications in this book. I believe learning rules before you understand concepts is frankly a waste of time. You may become frustrated or even give up because you believe the transaction is too complex.

Instead, I focus on the fundamentals of personal finance. I will show you how to keep it simple and how to do the simple things well. Of course, at some point, you will need to understand rules. But once you understand the basics properly, it’s much easier to follow the detailed rules.

Let’s say you want to take a mortgage. You should first understand what a mortgage is, how to decide what option is best for you, and how to estimate how much you can afford. Otherwise, it makes no sense for a lending officer to tell you about the details of the loan agreement, the potential tax deductibility of the interest, the incentives available for first-time homeowners, or the rights of the lender if you cannot repay.

Whenever I wish to use a financial product or perform a transaction, I check the detailed rules because they change often. I don’t memorize them. But how the transactions work and their concepts hardly ever change. Because I know these basics, I understand the current rules easily.

You can apply the principles and techniques from this book when you are earning income for the first time or if you are already in a bad financial situation. If you have experience, you may know some of the early material in the book. If so, focus on the areas you think are most relevant to your pain points. For example, if you have dependents, you may want to make Action 2: Protect Yourself and Your Dependents a priority. If your area of stress is too much debt, then Action 3: Manage Your Debt could give you immediate help. When you have greater peace of mind, then try to focus on the other areas. I still encourage you to read from the beginning because I’ve organized the content to build your knowledge in a logical way.

Why is this book different?

At the core, my focus is financial education. When you hear “education” you may think about school. Except you usually apply subjects you learn in school in specific circumstances, such as in your job. Whereas you’ll apply the financial lessons in this book every time you reach into your wallet/handbag or whenever you make a financial decision. I want to empower you to make wise choices. Or, if you choose a “bad” option, you know that you did because it was deliberate and empowered. And yes, you can do so, guilt free.

The principle I tried to apply to each topic and chapter was “Show How; Don’t Tell.” Have you ever read something and thought you had a lot of information but still had no idea what to do? That’s the problem I tried to tackle. I believe personal finance is about applying our knowledge to make everyday decisions about our money. I do share a lot of information, but I try to focus on what is practical and show you how to apply it. Be aware though, it is easier to show how with some topics, while others require a greater awareness of facts.

There is an endless supply of personal finance books. I read many when I was trying to get my own finances under control. After completing them, I often asked myself these questions:

To avoid these problems, my approach is to teach each topic. When I complete each one, you should have enough knowledge to act confidently. Think about a subject you learned at school, for example, math. You began by learning to count, then performed basic calculations, and progressed to complex equations. I try to use the same approach. I’ll build your knowledge slowly and gradually introduce the less straightforward areas.

You’ll notice my approach loosely follows our life stages. Once we begin to work, we immediately begin to face choices about our money. At this stage, many decisions will affect us for a long time if we get them wrong. Eventually, different life changes arise, creating further complexities such as marriage, children, and mid-life responsibilities. Then, suddenly the priority becomes planning for life when our best earning years are behind us.

Investing and retirement planning

I do not cover investing and retirement planning, which is different from many books on personal finance. In those books, large portions tend to focus on these two areas.

In my view, these are two advanced topics, and practically speaking, most of us cannot begin to think about them until we have enough surplus funds. If you struggle to make ends meet or debt is burdening you, your present problems are much more pressing. It would, therefore, be impossible to focus on investing and your retirement. You need to work yourself out of your current situation first. Even if you are less constrained, let’s say you just started your career, you will have many financial obligations to attend to before retirement.

I am not suggesting that you should not invest and plan for your retirement as early as possible. Quite the opposite: you absolutely should make it a priority. I am only being practical and recognizing that we often must balance this goal with other realities. Often, those other realities take greater priority.

My main objective, therefore, is to help build your knowledge, and show you how to apply it, to the point where you generate surplus funds. When you do so consistently, you can then focus on investing and detailed retirement planning. And frankly, most books cover these two topics in such a high-level way that they do not empower anyone to make a decision. It’s a lot of telling but not showing how.

When I help you to take control of your money successfully, I bet you’ll become much more interested in understanding how to invest and plan for your retirement.

Are you ready to begin? Let’s start at the end.

Decisions About Your Surplus

I hope you took a moment to celebrate if this was the first time you performed Steps 1 to 4. Celebrate a little more if you decided what actions you intend to take to correct a deficit. Remember, these are deliberate actions to take control of your finances. You are no longer “winging it” or living month-by-month. It’s an incredibly liberating feeling to know you are in control of your financial destiny!

Let’s continue with our second question from Step 3. There were two parts: (a) If I am in surplus, what should I do with it? And (b) What size of surplus should I aim for?

To answer part (a), I recommend using it in four ways:

- Build an emergency fund.

- Repay debt faster than scheduled.

- Save for medium and long-term goals.

- Invest and plan for retirement.

I expect for most of us our surplus is only large enough to focus on one goal at a time. This is fine and the list is in the order that I suggest you follow to put your surplus to work. For example, if you are currently completing 1 (building an emergency fund), do not start 2 (repaying debt more quickly) until you finish 1. If your surplus is large enough to allow you to tackle more than one goal at the same time, then definitely proceed. I am therefore answering the second question as well: what size of surplus should you aim for? You should aim for an amount that allows you, at a minimum, to achieve 1. When you complete 1, you should aim for an amount that allows you to achieve 2. And so on.

Let’s look at the four uses briefly, as we’ll meet them in more detail in the later chapters.

Build an emergency fund

This is essentially “rainy day” money. This means you set aside some funds in case the unforeseen happens. I cover this activity in the next chapter.

Repay debt faster than scheduled

Most loans have a fixed repayment schedule, and those that do not, have at least a minimum payment. The goal here is to pay more than the set payments until your loans are repaid.

Save for medium and long-term goals / Invest and plan for retirement

Did you notice that I put 3 and 4 together? I did this because we normally consider retirement planning as a long-term goal. But I like to treat retirement as a separate use of your surplus because it is important. I’ll cover this in more detail in our closing chapter The End of Our Journey, but for now, let me make two points:

- Although retirement planning is fourth on the list, whenever you have money that you are unlikely to need, you should use it for your retirement funds. I stress these must be funds you realistically do not intend to use.

- Retirement funds are what most individuals should use for investing.

Let me expand on the last point briefly until we return to this topic in the closing chapter. In my view, only the truly wealthy have enough money to have both a retirement pool and an investment pool. They generate large surpluses that easily meet their retirement needs, and the excess is available for other investments to build wealth. Of course, this wealth is also available during retirement.

Most of us, however, are not that fortunate. Our surplus funds are smaller, and we usually must work through the list I provided one-by-one. We only focus on retirement when 1 to 3 are under control and at this point, we allocate every available dollar to retirement savings. In our case, we have one pool of money: a retirement pool, which we invest.

Savings

Let’s spend a few moments discussing the concept of “Savings.” Did you notice that the action of “saving” only arises in the third use of your surplus? This is deliberate because it helps ensure the different uses of your surplus are clear.

The word “Savings” can be used in a general way, which does not necessarily mean the person doing the saving is becoming wealthy. So, to avoid any misunderstanding as we move forward with the Steps, let’s agree on what savings is definitely not.

What is not Savings?

Have you ever heard people say they are saving for a vacation, for Christmas presents, to buy a phone or a gaming system? We should find a unique way to describe this intent because the funds gathered for these uses are not part of our savings. Yes, you are setting aside money over a period to buy something. But these funds are for a current expense. As such, they are not part of your savings. To emphasize, these funds are to pay for a present Need or Want.

Recognizing that you are setting aside funds to meet a short-term Need or Want is important. It is easy to mislead yourself by thinking you are actively saving but feel disappointed when you aren’t more financially secure. But let’s acknowledge something important. Deciding to gather funds before spending is exactly the discipline you need to achieve financial freedom. The easy approach would be to buy the item using a credit card. You’ll learn in a later chapter that this is a bad financial decision. So yes, “saving” before you buy something is an excellent habit. My point is, do not consider these amounts as real savings.

What is Savings, and why are they important?

Real savings are for your medium to long-term benefit. They are what is left after you pay all outflows and allocate money for specific goals such as an emergency fund. You do not use real savings to meet day-to-day living expenses (Needs or Wants).

While the act of saving might seem like a short-term action, you should view it as part of a larger plan. Each month of savings adds up to a year, and each year builds over time. You use these accumulated amounts to meet your medium- term goals or invest for your long-term goals. Medium-term goals could include saving for a deposit on a home, higher education, or some other significant aspiration. Long-term goals could include children’s education or your retirement.

It is easy to believe an impulse purchase or loose spending only has a short-term impact. A different picture appears if you think it was money you could have saved to meet your long-term, and more important, goals.

For context, $1 saved today, continuously invested at 4% will become $2 (it will double) in around seventeen-and-a-half years. Think about that for a moment, with larger amounts instead.

Imagine how secure your future financial self could be if you save instead of spending in a way that has no lasting value beyond the present. The bottom line is your current spending decisions have a major impact on your ability to meet your future goals.

What is Savings used for?

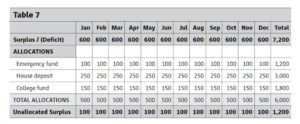

To summarize, when you actually “save,” you gather funds to achieve medium and long-term goals. In your 12-month estimate, these are included in the allocation lines at the bottom of Table 7 in Step 3, repeated here:

The “Surplus/(Deficit)” line at the top is the difference between your total inflows and outflows. From your surplus, you now allocate funds to meet specific goals. In the example, you’ll notice there were no specific allocations for retirement because there isn’t enough surplus. That’s unfortunate, but often a reality. In the example, this person would first have to gather funds for any current goals. After reaching that goal target, the person then begins to set aside funds toward a new goal, which could be retirement.

Maintain order

I previously recommended using a checking account as your financial center for day-to-day transactions. When you start to have regular surpluses, you’ll notice your bank account grows. Once this begins, to help keep things in order, you should separate true savings (your allocations) from day-to- day funds.

I suggest using a savings account to hold the funds you saved/ allocated. You can also use a savings account to hold funds you are setting aside for an upcoming purchase. Eventually, you’ll want to move your allocated funds to a long-term savings option. I’ll cover this approach in Action 6: Invest and Plan for Retirement. For now, use your savings account to hold the allocations. I’ll explain emergency funds specifically in the next chapter.

Wrap up

This was an important chapter. Having arrived at the key milestone of an estimated 12-month surplus, next, I’ll show you how to put that surplus to work. I suggested four uses and the upcoming chapters will explain each in detail.